Smarter Chargeback Management Starts Here

Credit is a promise to pay, not cash guaranteed to your business. Chargebacks are becoming more common, even in card-present transactions, and can result in costly fees, lost revenue, and serious financial impact.

While this may sound concerning, chargebacks can be managed — and often prevented.

Here Are Practical Tips to Help You Reduce and Handle Customer Disputes

What is a Chargeback?

This process is designed to protect customers, allowing them to easily dispute transactions for various reasons. However, merchants must provide proof that the transaction was legitimate, which requires significantly more effort.

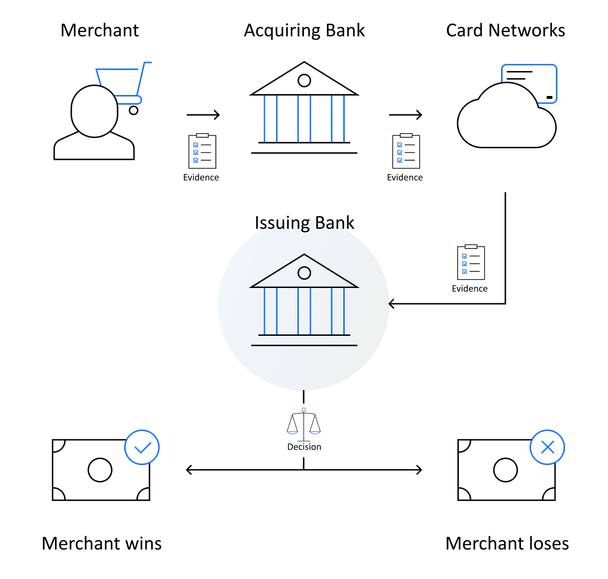

The Chargeback Process:

- Cardholder: Initiates the dispute and provides a reason (and transaction details based on the reason code).

- Issuing Bank: Receives the dispute, requests funds to be temporarily removed, and communicates updates to the cardholder.

- Payment Processor: Notifies you of the chargeback and provides a way for you to respond with evidence.

- Card Brands: Review all submitted information and make the final decision based on their rules and terms.

Reasons for Chargebacks

There is no way to eliminate chargebacks but knowing why and when chargebacks occur is a great way to counteract them. Here are the top 4 reasons for a dispute and how to reply.

- Fraud / Unauthorized Transaction: Submit a signed receipt, agreement, or invoice with the cardholder’s name, address, phone number, and transaction details. Matching ID or card copies can strengthen your case. These are difficult to win — especially for card-not-present transactions — so collect as much customer data as possible upfront.

- Merchandise / Services Not Received: Provide the agreement or invoice, signed documents, customer details, and proof of delivery or service. Include any post-transaction communication, especially if the customer requested a refund before disputing.

- Duplicate Processing: Review transaction records to confirm. If duplicate, accept the chargeback or show proof of refund. If not, provide evidence the customer authorized multiple purchases.

- Not as Described: Include agreements, transaction details, and directly address the customer’s complaint with supporting proof or documentation.

How to Win a Dispute?

Cardholders typically have up to 180 days to file a chargeback, while merchants usually have only 10–15 business days to respond. Keeping receipts and transaction records for at least 180 days can help you gather the necessary evidence to dispute a claim. It’s important to respond promptly with detailed documentation and a clear written explanation of the transaction.

There are a few outcomes to be prepared for:

- You win the dispute: You will receive a credit back to your account that was held while the dispute was ongoing. You will still incur a chargeback fee.

- You lose the dispute: The transaction is deemed invalid and you transaction amount that was held is returned to the cardholder.

What is a Retrieval request?

A merchant may request verification through their bank which can result in a fee to you the merchant and if you fail to respond it can result in a chargeback.